Parameter Dispersion (Variance-Covariance) Matrix

The dispersion matrix for the parameter estimates  is the matrix

is the matrix  , where

, where  is the covariance of

is the covariance of  and

and  . The dispersion matrix is calculated according to the formula

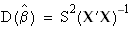

. The dispersion matrix is calculated according to the formula where S2 is the estimated variance, as defined above, and X and

where S2 is the estimated variance, as defined above, and X and  are the regression matrix and its transpose, respectively.

are the regression matrix and its transpose, respectively.

is the matrix , where is the covariance of and . The dispersion matrix is calculated according to the formula where S2 is the estimated variance, as defined above, and X and are the regression matrix and its transpose, respectively.