ESTIMATE_MISSING Function

Estimates missing values in a time series.

Usage

result = ESTIMATE_MISSING(tpoints, z)

Input Parameters

tpoints—Array of length n_obs containing the time points t1, ..., tn_obs at which the time series values were observed. n_obs is the number of non-missing observations in the time series. The time points must be in strictly increasing order. Time points for missing values must lie in the open interval (t1, tn_obs).

z—Array of length n_obs containing the time series values. The values must be ordered in accordance with the values in array tpoints. It is assumed that the time series after estimation of missing values contains values at equidistant time points where the distance between two consecutive time points is one. If the non-missing time series values are observed at time points t1, ..., tn_obs, then missing values between ti and ti+1, i = 1, ..., n_obs – 1, exist if ti+1 – ti > 1. The size of the gap between ti and ti+1 is then ti+1 – ti – 1. The total length of the time series with non-missing and estimated missing values is tn_obs – ti + 1, or tpoints(n_obs – 1) – tpoints(0) + 1.

Returned Value

result—Array of length (tpoints(n_obs – 1) – tpoints(0) + 1) containing the time series together with estimates for the missing values.

Input Keywords

Double—If present and nonzero, double precision is used.

Method—The method used for estimating the missing values:

If Method = 2 is chosen, then all values of gaps beginning at time points t1 + 1 or t1 + 2 are estimated by Method 0. If Method = 3 is chosen and the first gap starts at t1 + 1, then the values of this gap are also estimated by Method 0. If the length of the series before a gap, denoted len, is greater than 1 and less than  , then maxlag is reduced to len/2 for the computation of the missing values within this gap. Default Method = 3.

, then maxlag is reduced to len/2 for the computation of the missing values within this gap. Default Method = 3.

, then maxlag is reduced to len/2 for the computation of the missing values within this gap. Default Method = 3.Maxlag—A scalar value indicating the maximum lag number when Method = 3 was chosen. Default: Maxlag = 10

Mean_estimate—Estimate of the mean of the time series.

Convergence_tolerance—Tolerance level used to determine convergence of the nonlinear least squares algorithm used if Method = 2. Convergence_tolerance represents the minimum relative decrease in the sum of squares between two iterations required to determine convergence. Hence, Convergence_tolerance must be greater than or equal to 0.

Relative_error—Stopping criterion for use in the nonlinear equation solver used if Method = 2.

Maxit—A scalar value indicating the maximum number of iterations allowed in the nonlinear equations solver used if Method = 2. Default: Maxit = 200.

Output Keywords

Ntimes—Number of elements in the time series with estimated missing values. Note that Ntimes = tpoints(n_obs – 1) – tpoints(0) + 1.

Times_array—Array of length Ntimes = tpoints(n_obs – 1) – tpoints(0) + 1 containing the time points of the time series with estimates for the missing values.

Missing_index—Array of length (Ntimes – n_obs) containing the indices for the missing values in Times_array. If Ntimes – n_obs = 0, then this keyword is not valid.

Discussion

Traditional time series analysis as described by Box, Jenkins and Reinsel (1994) requires the observations made at equidistant time points t1, t1 + 1, t1 + 2, ..., tn. When observations are missing, the problem occurs to determine suitable estimates. ESTIMATE_MISSING offers 4 estimation methods:

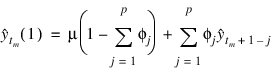

by μ the one-step-ahead forecast at origin

by μ the one-step-ahead forecast at origin  , can be computed by the formula:

, can be computed by the formula:

This value is used as an estimate for the missing value. The procedure starting with AUTO_UNI_AR is then repeated for every further missing value in the gap.

note | All four estimation methods treat gaps of missing values in increasing time order. |

Example

Consider the AR(1) process:

Yt = φ1Yt–1 + at, t = 1, 2, 3, ...

We assume that {at} is a Gaussian white noise process,  . Then, E[Yt] = 0 and VAR[Yt] = σ2/(1 – φ12) (see Anderson, p. 174).

. Then, E[Yt] = 0 and VAR[Yt] = σ2/(1 – φ12) (see Anderson, p. 174).

. Then, E[Yt] = 0 and VAR[Yt] = σ2/(1 – φ12) (see Anderson, p. 174).The time series in the code below was artificially generated from an AR(1) process characterized by φ1 = –0.7 and σ2 = 1 – φ12 = 0.51. This process is stationary with VAR[Yt] = 1. As initial value, Yt := a0 was taken. The sequence {at} was generated by a random number generator.

From the original series, we remove the observations at time points t=130, t=140, t=141, t=160, t=175, t=176. Then, ESTIMATE_MISSING is used to compute estimates for the missing values by all 4 estimation methods available. The estimated values are compared with the actual values.

maxlag = 20

times_1 = LONARR(200)

times_2 = LONARR(200)

x_1 = FLTARR(200)

x_2 = FLTARR(200)

y = [ 1.30540, -1.37166, 1.47905, -0.91059, 1.36191, $

-2.16966, 3.11254, -1.99536, 2.29740, -1.82474, $

-0.25445, 0.33519, -0.25480, -0.50574, -0.21429, $

-0.45932, -0.63813, 0.25646, -0.46243, -0.44104, $

0.42733, 0.61102, -0.82417, 1.48537, -1.57733, $

-0.09846, 0.46311, 0.49156, -1.66090, 2.02808, $

-1.45768, 1.36115, -0.65973, 1.13332, -0.86285, $

1.23848, -0.57301, -0.28210, 0.20195, 0.06981, $

0.28454, 0.19745, -0.16490, -1.05019, 0.78652, $

-0.40447, 0.71514, -0.90003, 1.83604, -2.51205, $

1.00526, -1.01683, 1.70691, -1.86564, 1.84912, $

-1.33120, 2.35105, -0.45579, -0.57773, -0.55226, $

0.88371, 0.23138, 0.59984, 0.31971, 0.59849, $

0.41873, -0.46955, 0.53003, -1.17203, 1.52937, $

-0.48017, -0.93830, 1.00651, -1.41493, -0.42188, $

-0.67010, 0.58079, -0.96193, 0.22763, -0.92214, $

1.35697, -1.47008, 2.47841, -1.50522, 0.41650, $

-0.21669, -0.90297, 0.00274, -1.04863, 0.66192, $

-0.39143, 0.40779, -0.68174, -0.04700, -0.84469, $

0.30735, -0.68412, 0.25888, -1.08642, 0.52928, $

0.72168, -0.18199, -0.09499, 0.67610, 0.14636, $

0.46846, -0.13989, 0.50856, -0.22268, 0.92756, $

0.73069, 0.78998, -1.01650, 1.25637, -2.36179, $

1.99616, -1.54326, 1.38220, 0.19674, -0.85241, $

0.40463, 0.39523, -0.60721, 0.25041, -1.24967, $

0.26727, 1.40042, -0.66963, 1.26049, -0.92074, $

0.05909, -0.61926, 1.41550, 0.25537, -0.13240, $

-0.07543, 0.10413, 1.42445, -1.37379, 0.44382, $

-1.57210, 2.04702, -2.22450, 1.27698, 0.01073, $

-0.88459, 0.88194, -0.25019, 0.70224, -0.41855, $

0.93850, 0.36007, -0.46043, 0.18645, 0.06337, $

0.29414, -0.20054, 0.83078, -1.62530, 2.64925, $

-1.25355, 1.59094, -1.00684, 1.03196, -1.58045, $

2.04295, -2.38264, 1.65095, -0.33273, -1.29092, $

0.14020, -0.11434, 0.04392, 0.05293, -0.42277, $

0.59143, -0.03347, -0.58457, 0.87030, 0.19985, $

-0.73500, 0.73640, 0.29531, 0.22325, -0.60035, $

1.42253, -1.11278, 1.30468, -0.41923, -0.38019, $

0.50937, 0.23051, 0.46496, 0.02459, -0.68478, $

0.25821, 1.17655, -2.26629, 1.41173, -0.68331]

tpoints = INDGEN(200) + 1

n_miss = 0

times_1(0) = tpoints(0)

times_2(0) = tpoints(0)

x_1(0) = y(0)

x_2(0) = y(0)

k = 0

FOR i=1L, N_ELEMENTS(tpoints)-1 DO BEGIN & $

times_1(i) = tpoints(i) & $

x_1(i) = y(i) & $

; Generate series with missing values

IF ((i NE 129) AND (i NE 139) AND (i NE 140) AND $

(i NE 159) AND (i NE 174) AND (i NE 175)) THEN BEGIN & $

k = k + 1 & $

times_2(k) = times_1(i) & $

x_2(k) = x_1(i) & $

ENDIF & $

ENDFOR

n_obs = k+1

times_tmp = times_2(0:n_obs-1)

x_tmp = x_2(0:n_obs-1)

FOR j=0L, 3 DO BEGIN & $

PRINT, "---- value of j is ", j & $

result = 0 & $

times = 0 & $

missing_index = 0 & $

IF (j LE 2) THEN BEGIN & $

result = ESTIMATE_MISSING( $

times_tmp, x_tmp, $

Method=j, $

Ntimes=ntimes, $

Times_Array=times, $

Missing_Index=missing_index) & $

ENDIF ELSE BEGIN & $

result = ESTIMATE_MISSING( $

times_tmp, x_tmp, $

Method=j, $

Ntimes=ntimes, $

Maxlag=maxlag, $

Times_Array=times, $

Missing_Index=missing_index) & $

ENDELSE & $

IF j EQ 0 THEN PRINT, "Method: Median" & $

IF j EQ 1 THEN PRINT, $

"Method: Cubic Spline Interpolation" & $

IF j EQ 2 THEN PRINT, "Method: AR(l) Forecast" & $

IF j EQ 3 THEN PRINT, "Method: AR(p) Forecast" & $

PRINT, ntimes, Format='("ntimes = ", I3)' & $PRINT, $

"Time Actual Predicted Difference" & $

n_miss = ntimes - n_obs & $

FOR i=0L, n_miss-1 DO BEGIN & $

miss_ind = missing_index(i) & $

PRINT, times(miss_ind), x_1(miss_ind), $

result(miss_ind), ABS(x_1(miss_ind) - $

result(miss_ind)), $

Format='(I3, ",", F13.5, ",", F13.5, ",", F13.5)' & $

ENDFOR & $

PRINT, '' & $

ENDFOR

Output

Method: Median

ntimes = 200

Time Actual Predicted Difference

130, -0.92074, 0.26132, 1.18206

140, 0.44382, 0.05743, 0.38639

141, -1.57210, 0.05743, 1.62953

160, 2.64925, 0.04680, 2.60245

175, -0.42277, 0.04843, 0.47119

176, 0.59143, 0.04843, 0.54300

Method: Cubic Spline Interpolation

ntimes = 200

Time Actual Predicted Difference

130, -0.92074, 1.54109, 2.46183

140, 0.44382, -0.40730, 0.85112

141, -1.57210, 2.49709, 4.06919

160, 2.64925, -2.94712, 5.59637

175, -0.42277, 0.25066, 0.67343

176, 0.59143, 0.38032, 0.21111

Method: AR(l) Forecast

ntimes = 200

Time Actual Predicted Difference

130, -0.92074, -0.92971, 0.00897

140, 0.44382, 1.02824, 0.58442

141, -1.57210, -0.74527, 0.82683

160, 2.64925, 1.22880, 1.42045

175, -0.42277, 0.01049, 0.43326

176, 0.59143, 0.03683, 0.55460

Method: AR(p) Forecast

ntimes = 200

Time Actual Predicted Difference

130, -0.92074, -0.86385, 0.05689

140, 0.44382, 0.98098, 0.53716

141, -1.57210, -0.64489, 0.92721

160, 2.64925, 1.18966, 1.45959

175, -0.42277, -0.00105, 0.42172

176, 0.59143, 0.03773, 0.55370