BOND_EQV_YIELD Function (PV-WAVE Advantage)

Evaluates the bond-equivalent yield of a Treasury bill.

Usage

result = BOND_EQV_YIELD(settlement, maturity, discount_rate)

Input Parameters

settlement —The date on which payment is made to settle a trade. For a more detailed discussion on dates see Chapter 8, Working with Date/Time Data in the PV‑WAVE User’s Guide.

maturity—The date on which the bond comes due, and principal and accrued interest are paid. For a more detailed discussion on dates see Chapter 8, Working with Date/Time Data in the PV‑WAVE User’s Guide.

discount_rate—The interest rate implied when a security is sold for less than its value at maturity in lieu of interest payments.

Returned Value

result—The bond-equivalent yield of a Treasury bill. If no result can be computed, NaN is returned.

Input Keywords

Double—If present and nonzero, double precision is used.

Discussion

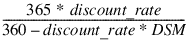

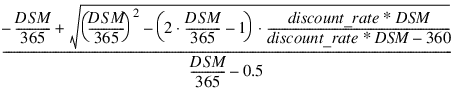

Function BOND_EQV_YIELD computes the bond-equivalent yield for a Treasury bill.

It is computed using the following:

If DSM ≤ 182:

otherwise:

In the above equation, DSM represents the number of days starting at settlement date to maturity date.

Example

In this example, BOND_EQV_YIELD computes the bond-equivalent yield for a Treasury bill with the settlement date of July 1, 1999, the maturity date of July 1, 2000, and discount rate of 5% at the issue date.

settlement = STR_TO_DT('7-1-1999', Date_Fmt = 1)maturity = STR_TO_DT('7-1-2000', Date_Fmt = 1)discount = 0.05

PRINT, BOND_EQV_YIELD(settlement, maturity, discount)

; PV-WAVE prints: 0.0528573

Version 2017.0

Copyright © 2017, Rogue Wave Software, Inc. All Rights Reserved.